A Multiple based approach to valuation of L&T Technology Services

A Multiple based approach to valuation of L&T Technology Services

With the overwhelming response to my first newsletter, I couldn't stop myself from writing the next issue. If you couldn't read it do check out the below link.

What is the First thing that comes to your mind when you hear the word L&T….

Construction, Govt. Projects, Real Estate, Manufacturing……right?

Yes, this is all correct because that’s what is their primary business when the company started in 1938 and for decades after that.

But, today it is actually a big conglomerate having very diverse interests in different industries. In fact, it has 3 IT services companies named L&T Infotech, L&T Technology Services, and MindTree (Since June 2019).

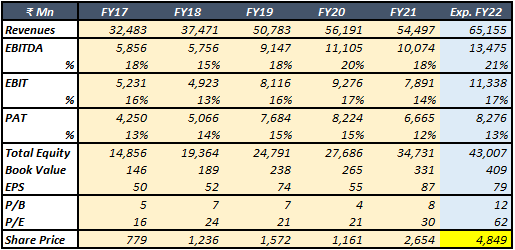

In this post, I will be analyzing one of the glowing gem of the L&T group which grabbed my attention after I saw this chart.

What does L&T Technology Services do?

The company identifies itself as a global leader in Engineering R&D services.

Some of its innovations include the world’s first autonomous welding robot, Solar ‘Connectivity’ Drone, and the smartest campus in the world.

Its expertise includes engineering design, product development, smart manufacturing, digitization. It also has over 69 innovation and R&D design centers globally. All these things collectively help it specialize in disruptive technology spaces such as 5G, Artificial Intelligence, Collaborative robots, Digital Factory, and autonomous transport.

Industries Served

The company has over 305 clients from very diverse profiles like

Industrial Products

Medical Devices

Consumer Electronics

Plant Engineering

Semiconductors

Telecommunications

Transportation

Media & Entertainment

Coming to geography, as of Jun-21, 62.3% of its revenues came from North America followed by Europe at 16.8% and India at 12.9%. The rest of the world contributed 8% of the revenues.

Also, as of Jun 2021, over 90% of the companies revenues were from repeat business.

Which speaks of its high customer retention rate.

But, all this is of no use if it’s not converting into profits. SoPast Performance

The company’s revenues have grown at 12.2% CAGR from the FY16-FY21 period.

At the same time, its EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization) has grown at a CAGR of 14.2%.

Profits after taxes, during the same period, have grown at 9.7% CAGR.

All this is quite decent but if we consider the effect of covid in the last 1.5-year performance, this looks impressive.

Additionally, as per management guidance, for the current fiscal year, revenues are expected to grow at 17.0% in dollar terms. Now, considering the rupee-dollar impact, this will surely give more than 17.0% growth in INR terms.

Valuation and Assumptions:

Based on the following assumptions about the next three quarters & as per management guidance…

The company should be able to grow revenue by 17.1% in INR and profits by 24.2% for the financial year.

Now,

Keeping the forecast in mind as well as the latest closing price. The company is currently valued at 62 times forward PE and 12 times Book Value. ( As on last closing price)

Now, looking at closing prices on 31st march and earnings for the years, this is one of the highest multiple the company has ever got. (See P/B and P/E row in the table above)

Technical Analysis:

Ever since it broke the resistance at 3000, the stock has been moving in the upward funnel. With immediate resistance at 5000 and support at a little above 4700 as per chart.

Now, the question is is this valuation multiple justified?

If no why and if yes how?

Why No?

It’s just too high compared to its past multiples.

Even if the company is poised to give all-time high performance, the valuations are way too stretched.

Current market interest rates are all-time low, when RBI starts to increase it, this will surely increase the cost of capital for the companies.

There can be further waves of covid, which can further delay CAPEX plans for private companies, thereby deferring deals for LTTS

Why Yes?

The company is one of the biggest pure-play Engineering R&D players in the world and any Covid wave should only accelerate plans for digitization for any industry once the wave resides. So, sooner or later this should benefit LTTS only.

Just like any other service-based company, LTTS also has almost negligible debt

As digitization grabs one industry, it will surely spread to other allied industries which will increase the overall market size for the ER&D industry. This will surely benefit LTTS as it is one of the biggest pure-play ER&D players in the world.

Additionally, there is a consensus that management might be conservative in its FY22 guidance and the company might even be able to surpass the guidance. Now, if this is going to happen the valuation might not be that high as earnings will also be higher with higher revenues

Conclusion :

The current market situation is justifying valuation more based on the emotional point of view about what can happen and might not be justified only based on fundamentals.

If you have any other reason or opinion about the current price of the company do let me know below in the comments section or on Twitter @daf_512.

Also, if you are interested to see more about the companies future plans you can check out the above link which is of their recent Investor Analyst Day.

Hi,

Did you like the analysis I have done above? If yes do subscribe to my newsletter so that whenever I write anything you will get it in your inbox. Additionally, you can share this with your acquaintances.

Also, if you want me to do any other type of analysis as well or cover some other topics or industries do let me know by comment.

Sources :